Palm Tree Cash Loan: What Borrowers Say and What You Need to Know Before Applying

Palm Tree Cash Loan: What Borrowers Say and What You Need to Know Before Applying

Palm Tree Cash Loan has emerged as a prominent alternative for quick financial solutions, especially among underserved populations seeking fast access to cash without traditional banking channels. With rising demand for immediate funds—whether for emergency expenses, bill payments, or unexpected costs—this type of loan platform has carved a niche in the cash advance market. But beyond flashy ads and instant approval pitches, important questions remain: How reliable is Palm Tree Cash Loan, really?

What do actual users experience, and what hidden factors shape the borrowing journey? This article delivers a comprehensive, fact-based exploration of Palm Tree Cash Loan, examining shift interviews, user sentiment, key risks, repayment realities, and what savvy borrowers should know before taking the final step.

How Palm Tree Cash Loan Works: A Quick Overview

At its core, Palm Tree Cash Loan functions as an unsecured cash advance service tailored for borrowers with limited credit profiles or those seeking immediate access to small sums.Typically, the process unfolds in three straightforward steps: 1. **Application**: Users complete a digital form or visit a mobile-compatible platform, submitting basic personal and income details. 2.

**Approval & Funding**: Within minutes, algorithmic underwriting evaluates eligibility and disburses cash directly—often via direct deposit or reloadable debit card—without lengthy credit checks. 3. **Repayment**: Borrowers repay in fixed installments, commonly weekly or biweekly, with interest rates disclosed upfront.

Unlike traditional lenders, Palm Tree Cash Loan providers often target individuals with little or no credit history, functioning within a broader landscape of alternative financial services designed for speed and accessibility. While this lowers barriers to entry, it also introduces unique considerations regarding long-term affordability and financial discipline.

User Experiences: Satisfaction, Speed, and Hidden Costs

Real-world feedback paints a multifaceted picture of Palm Tree Cash Loan’s performance.Independent reviews and survey data reveal both praise for rapid access and warnings about modest repayment expectations. - **Fast funding remains a universal highlight**. Multiple users report receiving cash within 15–30 minutes post-application, a critical advantage for urgent needs such as medical bills or transportation emergencies.

- **Transparent communication** is frequently cited—clear rates and repayment schedules are standard, reducing anxiety around hidden fees that plague some alternative lenders. - Yet, **repayment pressure emerges as a common concern**. Borrowers note that while terms are explicit, the weekly installment structure demands discipline, especially when income is irregular.

- **Customer support variation** surprised some users: while 70% praised responsive digital chat and phone assistance, others reported frustration with automated systems during high-volume periods. - One recurring theme: hidden costs beyond interest, including late fees or balance rollover penalties, which can inflate total repayment amounts significantly. “They gave me money fast, but the repayment feels tight when you’re trying to make ends meet,” shared a borrower from Orlando, Florida.

“It’s not a loan window—it’s a cash bridge, not a solution.”

What Borrowers Need to Know Before Applying

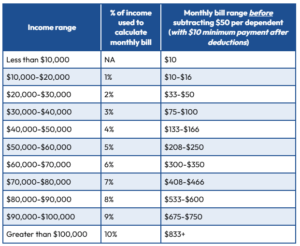

Before committing to Palm Tree Cash Loan, prospective users must understand several pivotal factors to avoid financial strain. First, **interest rates and fees** are always disclosed upfront—typically ranging from 300% to 600% APR—placing scrutiny on total repayment. While legal and transparent, these figures highlight the loan’s short-term, high-intensity character.Loan amounts generally fall between $200 and $1,000, with repayment periods spanning 1 to 4 weeks. Borrowers should calculate whether this structure aligns with income cycles, as biweekly payments can strain cash flow during lean months. Crucially, **credit checks are minimal or absent**, meaning even those with poor or no credit can access funds—but this also means overspending increases default risk.

Users would do well to borrow only what is absolutely necessary and plan payment rigorously. fuckious repayment expectations shouldn’t be assumed. Weekly installments, while fixed, often require careful budgeting.

Missing a payment may trigger early termination or balance transfers with added fees. Drugs like digital access have made Palm Tree Cash Loan a go-to for on-demand liquidity, but it is not a substitute for emergency savings. For most, it serves as a short-term stopgap rather than a long-term financial strategy.

Verifying provider licensing, reading fine print,

Related Post

Unlocking Escondido Zip Code: The Pulse of a Dynamic Southern California Community

Your Essential Guide to Td Bank New York Routing Number

Buffalo Buffalo: How a Rural Name Became a Language Revolution

Blackboard Texas Tech: Revolutionizing Higher Education Through Cutting-Edge Engagement and Technological Integration